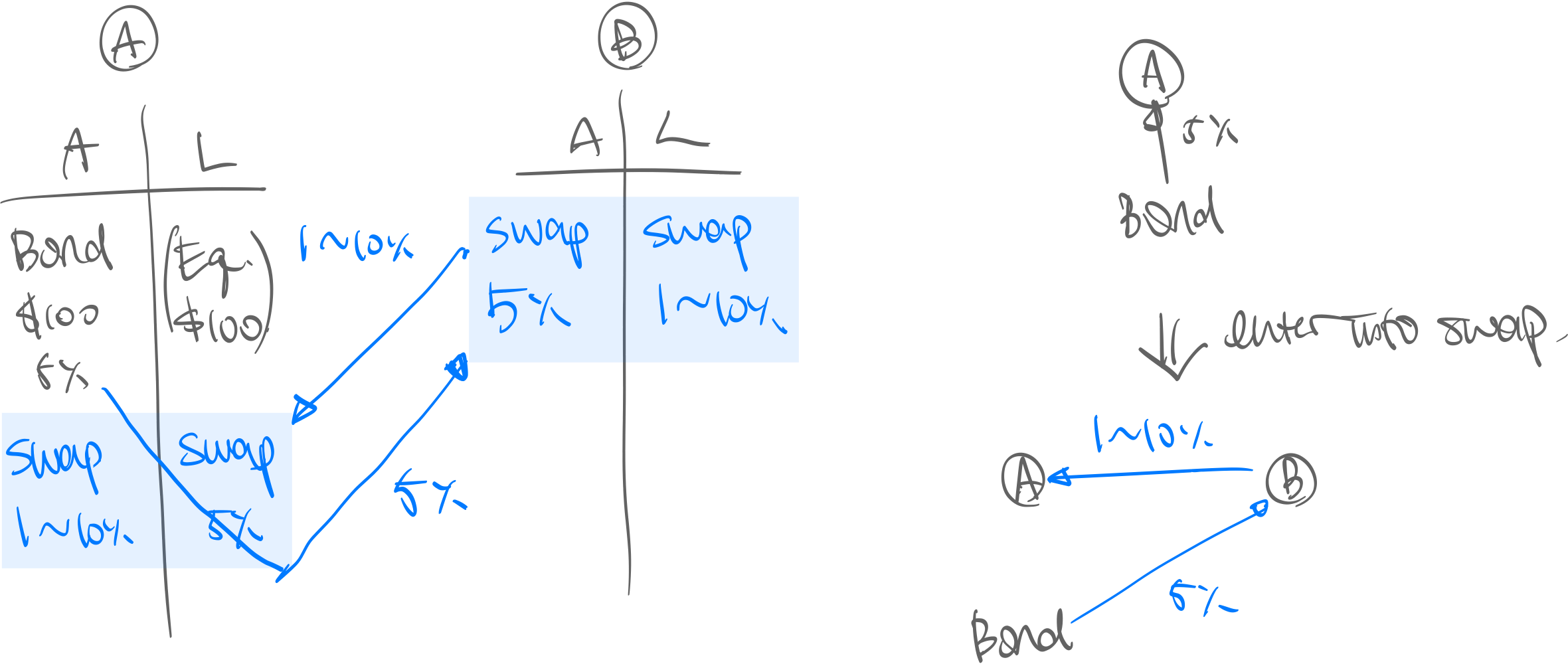

def. Interest rate swap is a financial instrument that can transform a floating rate to a fixed rate, and v.v.

- A holds a bond paying 5%

- A enteres into a IRS with B. They agree to redirect the fixed leg to B, and B will direct a floating leg to A.

- A earns floating 1~10%, and B earns the bond’s 5%.

- A retains ownership of the bond