General Equilibrium

Market Equilibrium is a point that is both optimal and feasible:

- Optimality: HHs, firms, govn’t are maximally happy; , maximized, government plan is in place

- Feasibility: Budget/Resource Constraints are in action

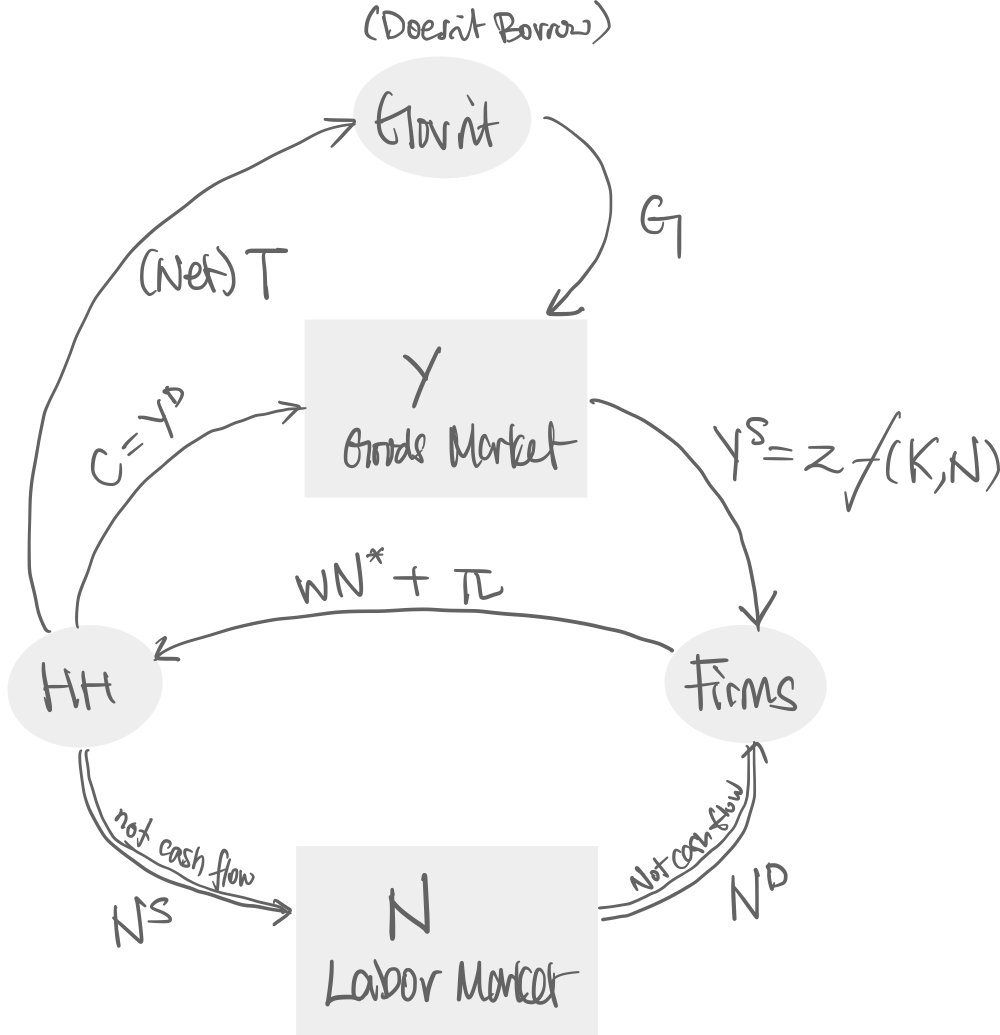

Feasibility

- Labor Market:

- Goods Market: ←“Resource Constraint”

- HH income: ←”Consumer Budget Constraint”

- Government ←”Government Budget Constraint”

⇒ If the two of three budget constraints are satisfied, the other one is automatically satisfied

Deriving the Equilibrium

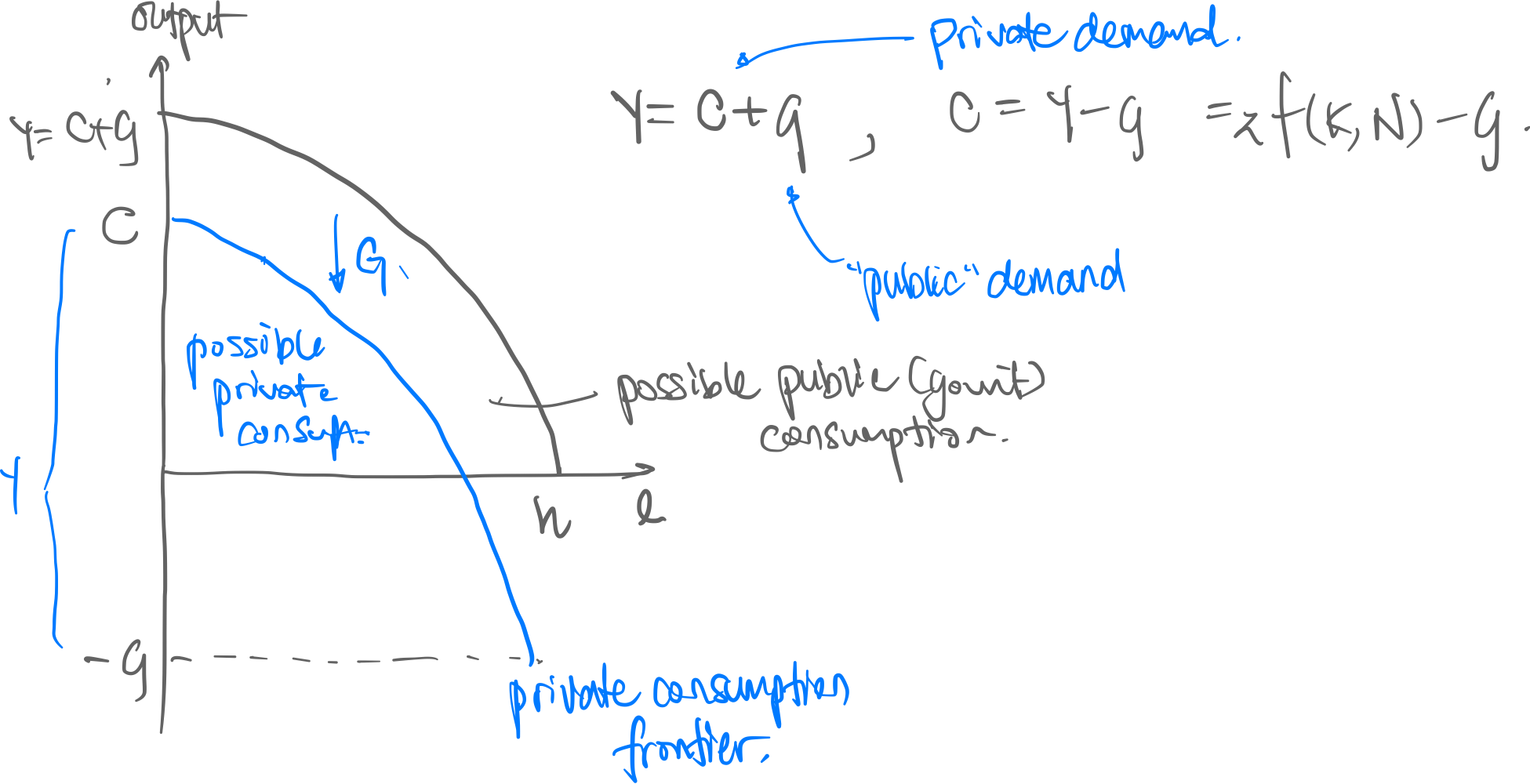

1. Production Possibility Frontier

- PPF indicates current level of technology, levels of govn’t spending

- Gradient of the PPF is the Marginal Rate of Transformation () of the economy; i.e. opportunity cost of transforming between consumption and leisure. This is equivalent to wage.

- Government speding is indicated by a downward shift of the PPF

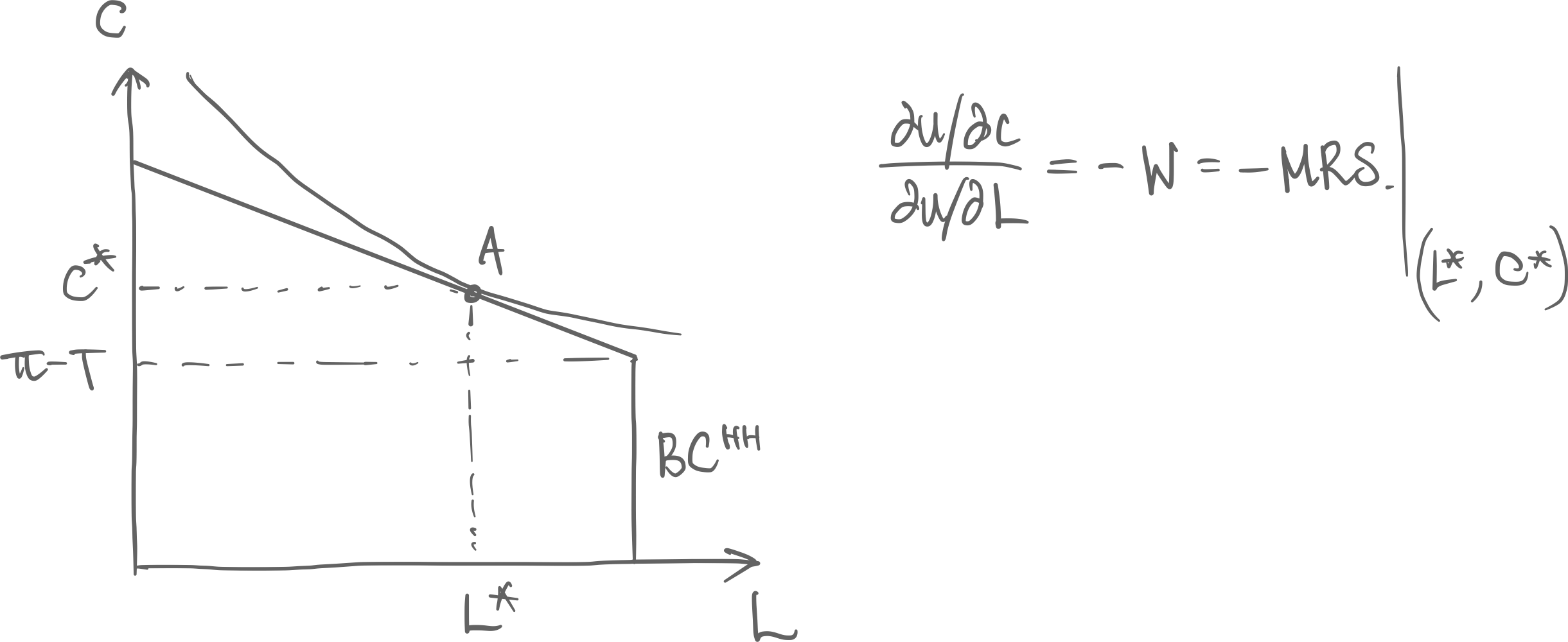

2. Household Optimization

- Consider: even if households do not work, they will get amount of income

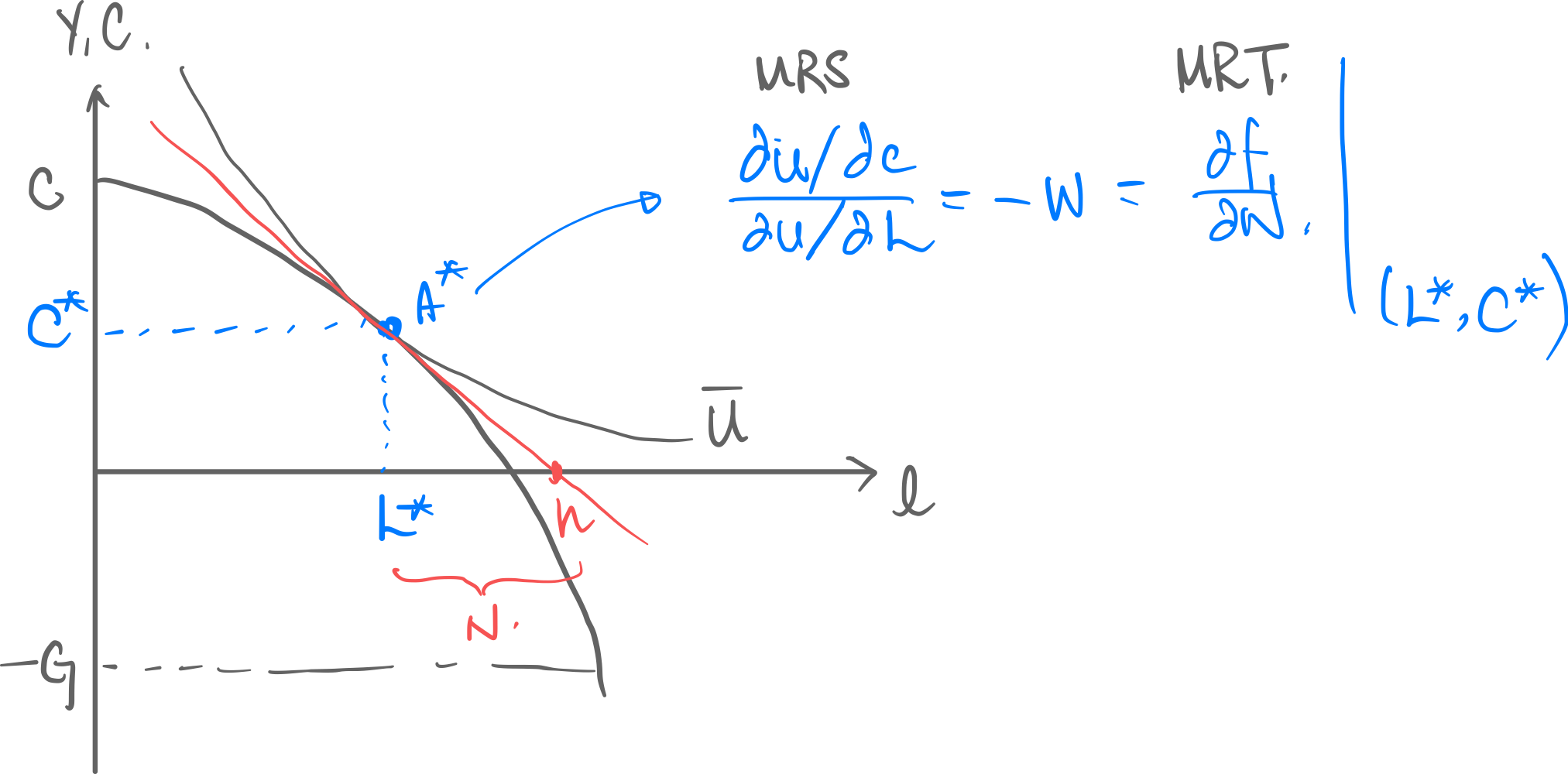

1+2: Market Equilibrium

At Point :

- Firms produce maximally, HHs maximize utility

- Is feasible [=inside PPF, inside HH budget constraint]

Examples of Disequilibrium

→ The left case: but is infeasible household indifference curve is outside → The right case: feasible, but household utility is not maximized

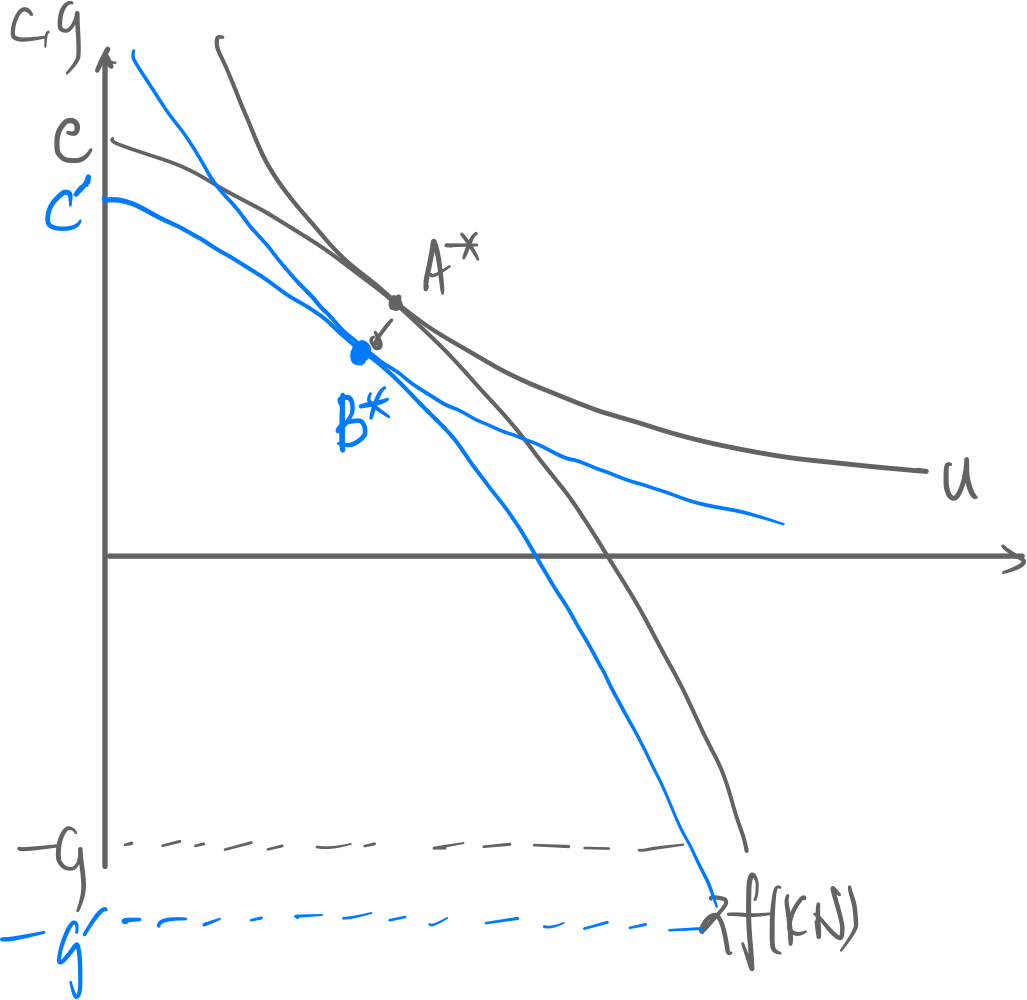

Changes in Equilibrium

- Changes in Government Spending [= ], normally due to war, or infrastructure projects

Government can crowd out private consumption, because it reduces HH income (income effect):

Taxes↑ ⇒ HH income ↓ ⇒ ↓ ⇒ ↓ ⇒ likely increases