Perfect Competition

Conditions:

-

Zero profit condition:

-

Pricing at marginal cost:

- ! only when is constant…

-

Theory of the Firm but with…

- Fixed costs, i.e.

- Firms will enter and exit

- ⇒ supply price and quantity is at

- → market price and individual firm’s quantity supplied are determined by this formula.

- This is equivalent to the minimum average cost condition .

-

Utility Maximization but…

- Consider only one good,

- There are more than one consumers.

-

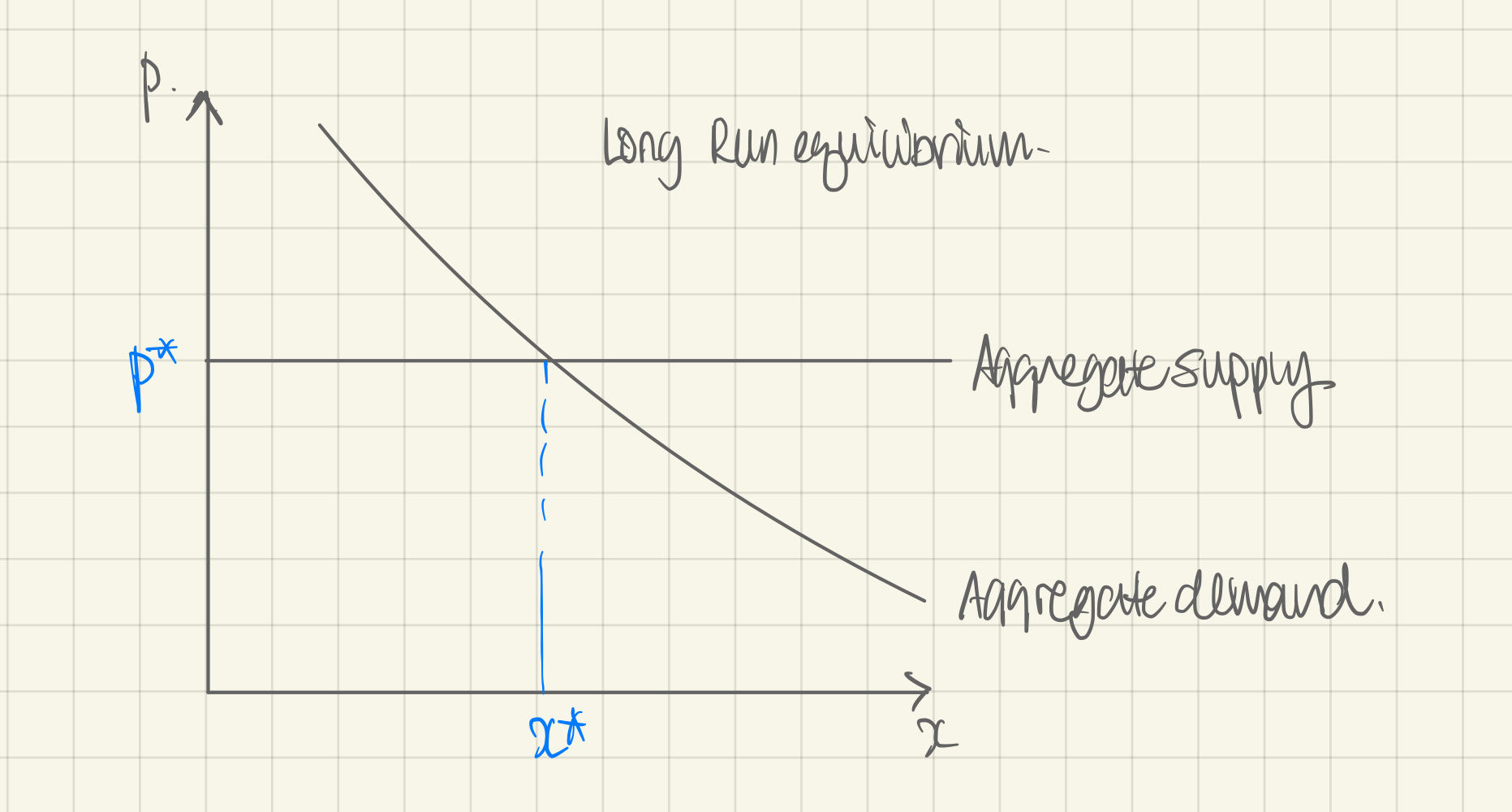

Market equilibrium:

- Price is set at because it is fully determined by the firm.

- The quantity supplied changes by firms entering and exiting (not by individual firms ramping up or cutting down on production!)

- Quantity demanded (=aggregate quantity supplied) of is fully determined by the consumer.

- Price is set at because it is fully determined by the firm.